Car Loans

How Much Car Can I Afford on a $500 Monthly Payment?

A $500 car payment can mean very different car prices depending on your rate, term, down payment, trade-in, and taxes. Here's the realistic math before you shop.

A $500 car payment sounds simple.

It is not simple.

That one number can mean a $23,000 car, a $30,000 car, or a $37,000 car. Same payment. Very different debt.

That is the trick with car loans. The payment is the headline. The loan term is the fine print wearing comfortable shoes.

Quick answer: a $500 payment usually means a $23,000 to $33,000 car

At 7.5% APR, a $500 monthly payment supports about $24,953 financed over 60 months.

APR means annual percentage rate. it is the yearly cost of borrowing money.

That $24,953 is not the sticker price. It is the amount you borrow after tax, fees, down payment, and trade-in.

Here is a real-world starting point.

With 7.5% APR, 7% sales tax, and $3,000 down, a $500 payment fits about:

| Loan term | Approx. car price | Amount financed | Interest paid |

|---|---|---|---|

| 60 months | $26,124 | $24,953 | $5,047 |

| 72 months | $29,830 | $28,918 | $7,082 |

| 84 months | $33,269 | $32,598 | $9,402 |

So yes, a longer loan lets you buy more car.

It also keeps you paying longer. Tiny detail. Only seven years of your life.

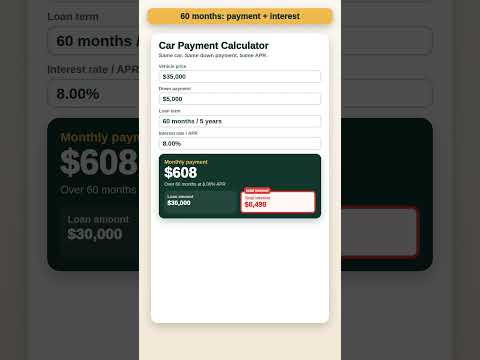

Use the calculator for your $500 car payment

Use the calculator above with a $500 target.

It starts near a $500 payment using a $29,000 car, $3,000 down, 72 months, 7.5% APR, and 7% sales tax. Change the price, APR, tax, down payment, trade-in, and term until the monthly payment lands where you want it.

If you want the full tool, use the Car Payment Calculator.

Here is the order I would use:

- Set the loan term first.

- Enter your expected APR.

- Add your sales tax.

- Add your down payment and trade-in.

- Move the car price until payment is about $500.

Do not start with the car you love. Start with the payment you can keep.

A dream car is fun. A dream car that eats your grocery budget is just a very shiny roommate.

What $500 buys at different APRs and loan terms

APR changes everything.

A low rate lets more of your $500 buy the car. A high rate sends more of your $500 to the lender.

Here is the financed amount a $500 payment supports.

| APR | 48 months | 60 months | 72 months | 84 months |

|---|---|---|---|---|

| 5.5% | $21,499 | $26,176 | $30,604 | $34,795 |

| 7.5% | $20,679 | $24,953 | $28,918 | $32,598 |

| 9.5% | $19,902 | $23,807 | $27,360 | $30,592 |

| 12.0% | $18,987 | $22,478 | $25,575 | $28,324 |

These numbers are loan amounts. They are not the out-the-door price.

Out-the-door price means the final price after taxes, fees, and dealer charges. It is the number that actually matters.

A dealer may show you a $500 payment on a $33,000 car. That does not mean the deal is good. It may mean the loan is long enough to need its own birthday cake.

Why the car price is lower than the loan amount

The loan amount and car price are not twins.

The loan amount is what you borrow. The car price is only one part of that.

Your financed amount may include:

- sales tax

- title and registration

- dealer document fees

- add-ons

- warranties

- gap insurance

- negative equity from your old car

Negative equity means you owe more on your old car than it is worth.

Example: your trade-in is worth $12,000, but you owe $15,000. That $3,000 gap can get rolled into the new loan.

Now your $500 payment is paying for the new car and the ghost of the old one. Very haunted. Very expensive.

At 7.5% APR for 72 months, $500 supports about $28,918 financed.

With 7% tax and no down payment, that points to about a $27,026 car.

With $3,000 down, it points to about a $29,830 car.

With $3,000 down and a $4,000 trade-in, it points to about a $33,830 car.

Same payment. Different story.

That is why you ask for the out-the-door price before you talk payment.

The 84-month trap: same payment, more debt

A longer loan can make an expensive car look affordable.

That is not magic. That is stretching.

At 7.5% APR, a $500 payment does this:

| Term | Amount financed | Total paid | Interest paid |

|---|---|---|---|

| 48 months | $20,679 | $24,000 | $3,321 |

| 60 months | $24,953 | $30,000 | $5,047 |

| 72 months | $28,918 | $36,000 | $7,082 |

| 84 months | $32,598 | $42,000 | $9,402 |

The 84-month loan gives you about $7,645 more buying power than the 60-month loan.

But it costs about $4,355 more in interest.

Interest is money you pay for the loan, not the car.

That extra $4,355 could be emergency savings, tires, insurance, or a vacation where nobody asks you about APR.

If you need 84 months to make the payment work, the car may be too expensive.

That is not a moral failure. It is math waving a small red flag.

Does $500 include insurance? Usually no

Most people say “$500 car payment” and mean the loan only.

Your real car cost is bigger.

A simple monthly example:

| Cost | Monthly amount |

|---|---|

| Loan payment | $500 |

| Insurance | $160 |

| Gas | $140 |

| Maintenance and tires | $75 |

| Total monthly car cost | $875 |

That $500 car can become an $875 car fast.

This matters because lenders care about approval. You care about living.

The lender may approve the payment. Your budget still has to survive rent, food, utilities, childcare, savings, and all the tiny charges that act innocent until the debit card starts wheezing.

Before you sign, put the full car cost into your budget. Use $500 for the loan, then add insurance, gas, maintenance, and registration.

If the full number feels heavy, believe it.

How much income do you need for a $500 car payment?

A decent rule is to keep total car cost under 15% of take-home pay.

Take-home pay means the money that actually lands in your bank after taxes and deductions.

If your full car cost is $875 per month, the 15% rule says you need about $5,833 per month in take-home pay.

At a 20% stretch, you need about $4,375 per month.

Here is the quick math:

| Monthly car cost | 15% target income | 20% stretch income |

|---|---|---|

| $500 loan only | $3,333/mo | $2,500/mo |

| $700 all-in cost | $4,667/mo | $3,500/mo |

| $875 all-in cost | $5,833/mo | $4,375/mo |

This is why the payment alone can lie.

A $500 payment may be fine for one household and brutal for another. Same car. Different rent. Different debt. Different life.

Personal finance gets a lot less personal when people ignore the person.

How to shop with a $500 limit

Walk into the dealership with rules before they hand you theirs.

Use this script:

“I am shopping by out-the-door price, not monthly payment. Please show me the full price, APR, loan term, total interest, taxes, fees, add-ons, and total of payments.”

Then ask these questions:

- What is the out-the-door price?

- What APR am I getting?

- How many months is the loan?

- What is the total interest?

- What is the total of payments?

- Are any warranties or add-ons included?

- Is negative equity rolled in?

- Is there a prepayment penalty?

A prepayment penalty means you pay a fee for paying the loan off early.

Most people do not ask these questions because nobody teaches them to. Dealers know that. The monthly payment becomes the magician’s handkerchief. Everyone watches it while the real cost disappears.

You do not need to be rude. You just need to be harder to confuse.

What to check next

Before you decide a $500 payment is safe, check these numbers:

- Run the payment in the Car Payment Calculator.

- Compare 60, 72, and 84 months.

- Add sales tax and dealer fees.

- Add insurance, gas, and maintenance.

- Check your trade-in value outside the dealership.

- Get a loan quote from a bank or credit union.

- Read the total interest before you sign.

If the dealer says, “What monthly payment are you trying to hit?” you can answer.

But do not stop there.

Say, “$500, and I also want to see the full loan cost.”

That second sentence is where the money is.

Bottom line

A $500 car payment can be reasonable.

It can also be a costume for a bad deal.

At 7.5% APR, $500 supports about $24,953 over 60 months or $28,918 over 72 months. With tax and $3,000 down, that is roughly a $26,000 to $30,000 car.

If you stretch to 84 months, you can buy more car. You also pay about $9,402 in interest at 7.5%.

The better move is simple.

Pick the term first. Estimate the APR. Add tax and fees. Add insurance and gas. Then choose the car.

That way, the payment serves your life.

Not the other way around.

Frequently asked questions

How much car can I afford with a $500 payment?

At 7.5% APR, a $500 payment supports about $24,953 financed for 60 months or $28,918 financed for 72 months.

After 7% tax and $3,000 down, that points to about a $26,124 car at 60 months or a $29,830 car at 72 months.

What car price is a $500 payment for 60 months?

At 7.5% APR for 60 months, $500 supports about $24,953 financed.

With 7% tax and $3,000 down, that is about a $26,124 car before dealer fees.

Is $500 a month a lot for a car payment?

It depends on income and other costs.

If $500 is only the loan, add insurance, gas, and maintenance. A $500 loan can become $875 per month all-in.

If that full cost is more than 15% to 20% of take-home pay, it may be too heavy.

Does a $500 car payment include insurance?

Usually no.

A car payment normally means the loan only. Insurance is separate. So are gas, repairs, tires, registration, and parking.

Should I choose 60, 72, or 84 months?

Choose the shortest term that fits your real budget.

At 7.5% APR, a $500 payment for 60 months costs about $5,047 in interest. At 84 months, it costs about $9,402.

The longer loan lowers pressure today but raises the total cost.

What if my APR is 12%?

At 12% APR, $500 supports about $22,478 over 60 months or $25,575 over 72 months.

Higher APR means less of your payment buys the car. More goes to interest.

Can a trade-in help me afford more car?

Yes, if the trade-in has positive equity.

Positive equity means the car is worth more than you owe. If your trade-in is worth $8,000 and you owe $3,000, you have $5,000 that can lower the new loan.

If you owe more than it is worth, that gap can make the new loan worse.